|

| Source: Wall Street Journal |

Desperate times call for desperate solutions. This could be Cyprus`s motto during the current period as one problem seems to follow another. On Monday morning, the Eurogroup reached a decision concerning the island`s future; one which will bring new meaning to words "economic depression". Most commented was the decision to impose capital controls, fearing a bank run or a flight of capital from the island.

Most believe that imposing capital controls essentially forces Cyprus out of the currency union (for example Frances Coppola, Pawel Morski, Tim Duy and Paul Krugman seem to share the same opinion). From my (limited) understanding of the subject this occurs because having euros in Cyprus means that they cannot be used in any way their holder wishes. Thus, if one cannot spend a euro in Cyprus but can do it in Germany this means that the latter euro is more valuable than the former since it can be used. Nevertheless, it seems that that the Cypriot authorities were out of options. If they did not control the outflow of capital from their country then soon a liquidity crisis would be forced on their banks. Was there anything else to do?

The only alternative that I am aware of is the one proposed by Guntram Wolff at Bruegel. His point is that the ECB should provide liquidity to all Cypriot banks in the case of a bank run. Nevertheless, the viability of this idea appears to be somewhat vague: if this was an option why did the EU policymakers not propose it during last Monday`s Eurogroup, even if it is after the Cyprus Parliament`s decision to impose capital controls? Did the Eurogroup leaders or most importantly Mario Draghi and his other colleagues present at the summit had no idea about the economic impact of these measures?

Under the recent decisions, Cyprus is de facto out of the euro. Karl Whelan (just like most of us) believes that the Eurozone is in the same situation as the US in 2008, when Hank Paulson decided to "roll the die" and let Lehman Brothers collapse; realizing that this was a terrible decision took a bit longer, just when AIG and almost every major bank in the US was about to collapse.

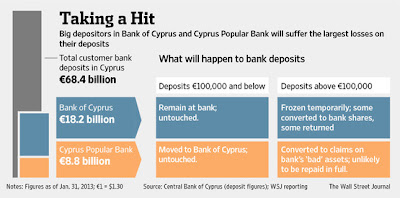

Aside the macroeconomic policies gone bad because politicians chose the wrong time to appear tough, banking decisions were bad as well: Bank of Cyprus PLC, currently receiving about €1bn from the ECB`s ELA will assume the responsibility of repaying Laiki`s €9.5bn after the latter`s division and merge with the former. In essence, Bank of Cyprus is receiving approximately €2,9bn of assets and liabilities with a responsibility of paying €9.5bn. It is the same idea as if a mother lends her 2 boys €10 each, the first boy loses them and the mother asks €20 from the second to cover her losses. Does not really make any sense does it? Cannot help wondering whether the Cypriot Central Banker, (who justified his first name (PANICos) through his comments on international media sources) understood that he was guaranteeing €9.5bn to give it to a bank with assets less than three times that (for those in the Central Bank who did not know, they have to guarantee every single euro they receive from the ELA. This essentially makes the state liable to pay for anything the banks cannot). How long will it really take for a bank assuming €9.5bn of ELA debt and €2.9bn of assets to repay? Too long indeed.

Next in realm of bad Cypriot decisions, comes the one which probably tops them all: selling Cypriot banks` subsidies in Greece. As I have explained before, the fact that Cypriot banks had subsidies in Greece made Cyprus systemic. Now, the island is just cut off of any possible systemic danger it could present to the EU (other than pure psychological ones); not to mention that even the price was ridiculous: at least €15bn of assets sold for just €524m (as recent sources state)!Out of all bad decisions this one really wins the gold: making the country un-systemic and getting a very low price simultaneously.

Depositors are not really going to be better off either: Out of the €8,8bn deposits that Laiki bank has, only €2,9bn are secured. This means that only they will be saved. Now, I cannot claim to be an expert in bank restructuring yet if NPL`s are just €2,3bn according to recent calculations, why aren`t just NPL`s transferred to the "bad" bank so that Laiki can continue its operations as a smaller bank, preserving much more wealth and jobs? Not to mention Laiki`s uninsured depositors who will probably wait for more than a decade to get some of their money back, as previous experience has shown. In addition, the percentage of uninsured deposits in the Bank of Cyprus which will be haircutted is still unknown. It was first considered to be 20%, then increased to 30% and now rumours speak of 40-50%. Whatever the amount might be, it will be no good if it is not used as cash (i.e. move from the banks to the Central Bank and then back to the banks in exchange for shares).

|

| Source: The Wall Street Journal |

Estimates claim that a more than 20% reduction in output is to be expected in Cyprus. The combined effects of capital controls, mistrust in the system and the banks, increased labour costs and high unemployment will mean that it would probably take until 2016 for the island`s GDP to stop contracting. Hugo Dixon estimates unemployment to reach 26% using Okun`s law (i.e. 0,5% increase in unemployment for every 1% decrease in GDP). The Eurogroup did not even recollect on its own mistakes: GDP contraction means less revenue for the government and leads to a vicious cycle of more austerity and less revenue.

Thus, what makes a Cyprus exit bad for the island? The cost of a Cyprus exit for the Eurozone countries is estimated at about €27.5bn, or €37.5 if you include the €10bn bailout from the EMS (considering an additional €11,5bn of ELA money this will make the amount €48bn). Yet, it is most likely that Cyprus will still honour the majority of its debt even if it is out of Eurozone. The outcome for the Cyprus economy is expected to reach about 15%. Most of this contraction will be due to the increased oil prices in the economy, a cost which could potentially be shifted to the state, via less taxation and less profit to the electricity provider. A Eurozone exit is obviously not a pretty scenario as it would entail risks we are currently unaware of. Yet, with capital controls already imposed in the island, the currency union is already history.

However this is more than economics now: The decision to leave the Eurozone is more about dignity and respect than anything else. Especially if you feel like your "friends" and "allies" have betrayed you, and you know that things will probably go equally bad economic-wise whether you leave or remain in the Eurozone. Even if Cyprus remains in the Eurozone, another plan will have to be drafted soon, as this will not be the end of the story (Alex Apostolides explains this thouroughly here).

The next day finds the whole of Europe astonished by the severity of measures imposed on an economy which represents just 0,2% of the Eurozone`s GDP. Yet, the precedent is set: Jeroen Dijesselbloem, has explicitly stated that a precedent on crisis management has been set. Every bank in the Eurozone is currently under threat. Every depositor, with more than €100,000 in his bank account will worry that if, or when, his bank faces trouble, his money will be lost. Trouble is not over for the Eurozone yet. Yet, although the water may be still in the surface, turbulence will exist in the deep; when trouble arises again (be it Italy or Spain or any other nation for that matter) panic will be set in the hearts of big depositors. The biggest bank run in history will occur. Then, capital controls will have to be implemented in the whole of Eurozone because people will be more afraid of their banks than of anything else.

Congratulations Eurogroup: you have opened Pandora`s box and you have shut out hope.